CDA S.A.

Small profitable and growing net income by 20%

currency: pln

market cap: 230M (57M USD)

shares price: 22.4pln

shares outstanding: 10.3m

2023 Pe ratio: 9.5

ev: 210M

ticker: CDA.NC

CDA is a Polish company that owns the cda streaming platform, which allows users to post their own materials and, as part of the premium service, offers access to many films and series from which the company earns 90% of its revenues.

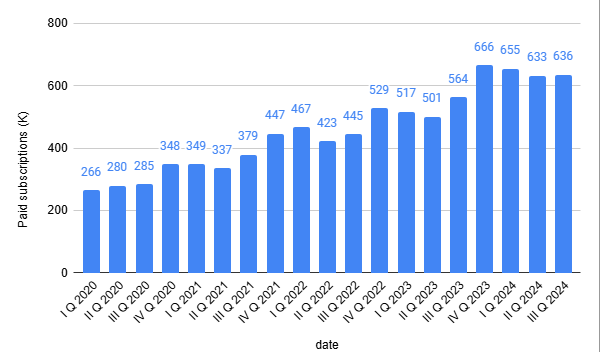

Your first thought would be to ask whether such a service is viable given the existence of Netflix. Because of offering many local films and series available only on the platform and a relatively low subscription price of 24 PLN (ca. 6 USD) per month, the company was able to grow its subscriptions count.

Subscription count has tendency to rise sharply in 4Q and be lower in second and forth quarters. It’s because in warmer months people tend to spend more time outside. Although this decrese is not that big it is still worth mentioning.

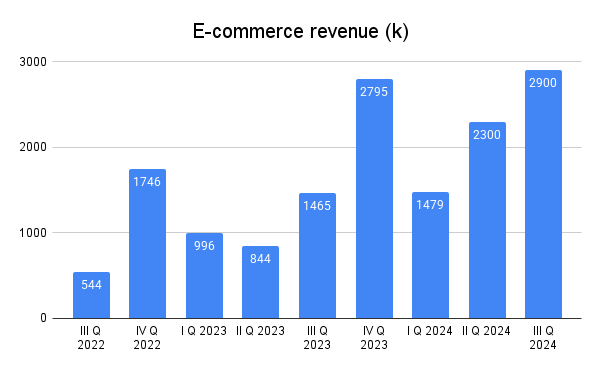

Besides core business the company also engages in e-commerce activities, which are growing rapidly and should constitute approximately 10% of this year’s revenue (with last quarter being the best in terms of revenue).

The company's e-commerce activity consists in selling accessories related to the universe of Kapitan Bomba (captain bomb) in its online store, an animated series to which the company bought the copyright in 2020.

Why does this opportunity exist?

The main reason is liquidity and free float of approximately 3%. In Poland, in order to perform a compulsory buyout, 95% of the votes is needed, which may be concerning considering that two main owners account for 97% of the shares. However, the buyout scenario is unlikely due to the history of minority shareholders treatment and the fact that the brothers have had many opportunities since the debut to take the company off the stock exchange. Nevertheless, it is a risk that should be taken into account.

Amendment to the copyright law, which resulted in a large drop in price in the first half of last year. Pursuant to the Act, the company is obliged to transfer a fee to ZAIKS, which is an organisation distributing collected fees to artists whose works are commercialy used. It is estimated that the costs of the fee will amount to approximately PLN 2-3 million per annum. To add insult to injury ZAIKS in December issued a demand for payment of approximately PLN 11 million for the period from January 1, 2015 to September 31, 2024. Although at first glance the value of 1/3 of the profit raises concerns, in fact it is not certain whether the company will have to pay it at all. Due to the fact that the act referred to by Zaiks came into force in September 2024 for the demand to be effective, it would have to be assumed that the law would apply retroactively, therefore I believe that the risk of payment is negligible and the company will probably enter into a court dispute, the cost of which I assume to be at most PLN 0.5 per year. . However, it should be bear in mind that such a process may take several years and and although the company as of 3Q report posseses around 20M of cash and is able to satisfy ZAIKS’s claim it still would impact the company negatively.

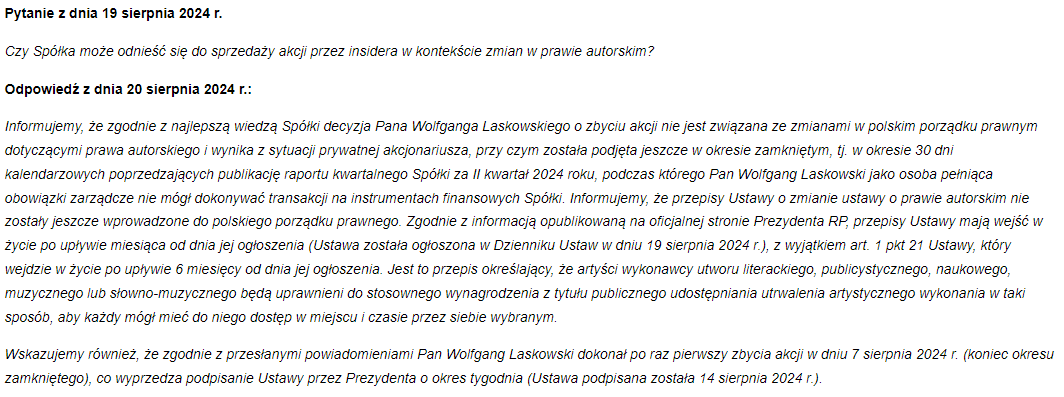

Due to its illiquid nature even small amount of selling pressure is enough to keep the price depressed for time ranging from couple of weeks or years at the end. And that’s exactly what is occuring. Wolfgang Laskowski (board representative for service development and press spokesman) who his shares received as part of an incentive program. Began selling his shares in August 2024 the number of shares he has already sold is 31,363 (as of 01.29) which is roughly 10% of free float. So it’s easy to image why stock price remains in consolidation. The company in answer to shareholder said that Wolfgang is selling because of personal reasons and not because of fear of potential legal risks.

source: https://spolka.cda.pl/lad-korporacyjny/pytania-od-inwestorow

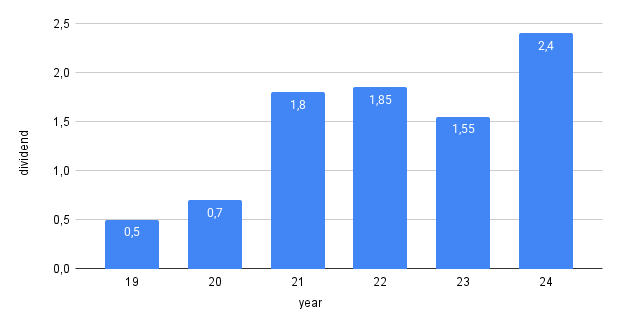

Dividend

The company since it began its journey on stock exchange has continuously paid out dividends.

Unfortunetly in June the company decided to halt dividend indefinitely. It was due to lack of knowledge of potential costs of new legislation. Now that the costs can be aproximated and met with cash possesed by the company, it is highly propaple that the company could reinstate dividend this year.

Catalyst

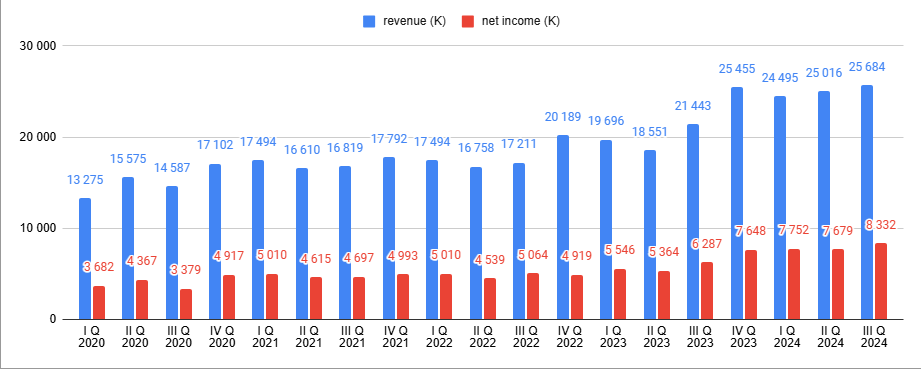

Maybe it is naive but I think annual report for fy 2024 released on March, 11 which I think should show net income of ca. 32M a Pe ration of 7 for a company with net income cagr for the last 5 years north of 20% is enough for the stock to trade significantly higher in the long term. Together with posible return to dividend payments should remind investors of true value of CDA.

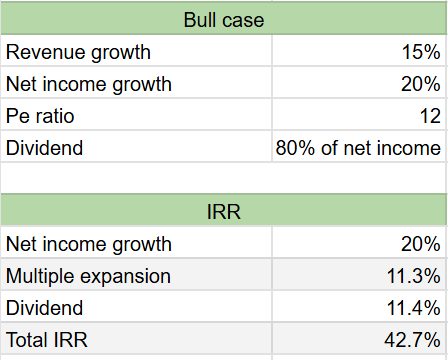

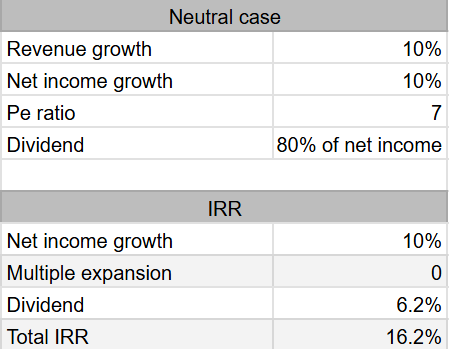

Scenarios

In each scenario I assume 5 years period and legal conflict resulting in payment by CDA of 11M pln which should be payed by existing cash reserves.

Bull case

Assuptions:

Growth maitained.

dividend reinstated.

Pe Ratio rerates to 12.

Neutral case

Assuptions:

Growth slows down.

Pe ratio stays the same.

dividend is halted for 2 years.

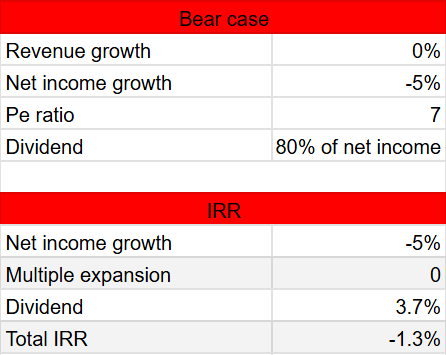

Bear case

Assumptions:

Negative growth.

Pe ratio stays the same.

dividend is halted for 2 years.

Summary

Cda is very cheap capital light business with 2024 estimated Pe ratio of 7 and net income growth of over 20%. But it’s iliquid and troubled by sale presure by one of big shareholders (in comparision to free float).

Thank you for reading if you enjoyed consider subscribing.

The article is not financial advise and should be viewed as author’s private opinon only.